Most PCI DSS hosting advice starts in the wrong place. It tells you to find a provider that says “PCI compliant,” then implies the hard part is done.

It isn't.

A hosting provider can deliver a strong security foundation, but PCI DSS compliant hosting is not the same thing as merchant compliance. If your team runs the payment application, installs plugins, approves third-party scripts, manages remote admin access, or stores cardholder data after authorization, your responsibilities don't disappear because the infrastructure sits on hardened servers.

That gap is where teams get hurt. They buy the right environment, assume it covers the full obligation, and discover too late that PCI DSS is enforced across infrastructure, systems, applications, access, operations, and documentation. Hosting matters a lot. It just doesn't cover everything.

The Compliance Myth That Costs Businesses Millions

The most expensive mistake in this space is simple. A business chooses a provider that advertises PCI-ready or PCI-compliant hosting, then treats that purchase like a certificate for the whole stack.

That's not how PCI DSS works. The merchant must meet all 12 core requirements, even when using a qualified provider, and 58% of SMBs pay non-compliance fees because they misunderstood shared responsibility and assumed provider certification covered their entire environment according to PCI DSS Guide's discussion of PCI compliant hosting responsibilities.

What teams usually misunderstand

The host may secure the facility, hypervisor, perimeter controls, and core server baseline. Your team still owns what you install and how you operate it.

That includes things like:

- Application maintenance: Your ecommerce platform, custom checkout code, CMS plugins, and payment extensions still need patching and review.

- Third-party script control: If marketing tags or support widgets touch the payment page, someone on your side must validate and govern them.

- User access decisions: The host can provide MFA mechanisms and account controls, but your team decides who gets access and whether that access remains justified.

- Operational evidence: PCI DSS isn't just security. It's also proof. Somebody has to retain records, approvals, reviews, and change control artifacts.

Practical rule: If your staff can log in, configure it, install it, approve it, or ignore an alert from it, you probably still own part of the PCI obligation.

What works and what fails

What works is treating hosting as one layer in a compliance program. Pick an environment that supports segmentation, logging, access control, and evidence retention. Then map every requirement to a named owner.

What fails is the vague sentence I still see in too many buying discussions: “Our host handles PCI.”

A provider can support PCI DSS. A provider can reduce your scope. A provider can take over operational work if managed services are clearly defined. But automatic compliance doesn't exist. If no one on your team can answer who owns scripts, patches, admin access, quarterly scans, and incident response coordination, you're already in the danger zone.

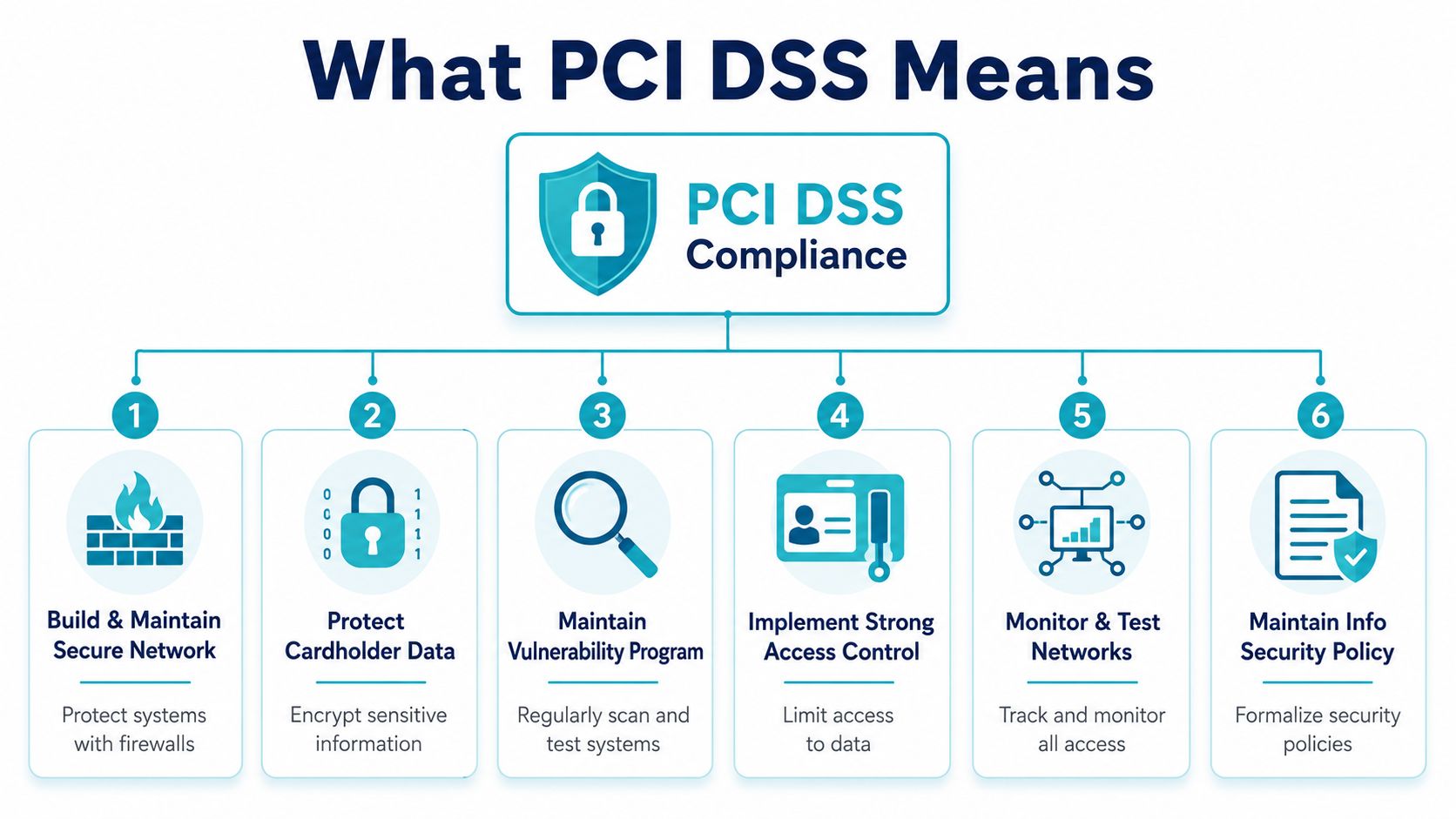

What PCI DSS Compliance Actually Means for Hosting

PCI DSS is easier to understand when you stop treating it like a marketing badge and start treating it like building code for payment systems. The standard sets baseline controls for any organization that accepts, transmits, or stores cardholder data. It applies whether you process a massive payment volume or only a small number of transactions.

The structure matters. PCI DSS organizes 16 specific requirements into six control objectives, including protecting stored cardholder data, encrypting transmission across open public networks, maintaining vulnerability management, enforcing access control, monitoring systems, and maintaining an information security policy, as summarized by Colocation America's overview of PCI-compliant hosting requirements.

The framework in plain English

A compliant hosting environment must help you do six things well:

- Secure the network perimeter

- Protect cardholder data in storage and transit

- Reduce known vulnerabilities

- Limit access to only what's necessary

- Track and test what happens in the environment

- Run security as an ongoing operating discipline

That's why PCI DSS hosting discussions that focus only on SSL certificates or firewall presence miss the point. The standard isn't asking whether a provider has a secure-looking product page. It's asking whether the environment supports disciplined control over data, access, logging, segmentation, maintenance, and policy.

Compliance levels affect validation, not relevance

PCI DSS categorizes organizations into four compliance levels based on annual transaction volume, and Level 1 covers entities processing over 6 million transactions per year and requires an annual audit by a Qualified Security Assessor (QSA), according to Microsoft's PCI DSS compliance offering documentation. Lower levels have different validation paths, but that doesn't mean the security obligations disappear for smaller merchants.

That distinction matters because many smaller businesses think PCI only becomes serious at enterprise scale. It doesn't. The validation method may differ. The duty to protect cardholder data doesn't.

Hosting only makes sense when the controls are usable

A good PCI-capable hosting environment isn't just hardened. It's operationally workable. Your team should be able to define scope, isolate payment systems, manage access, and produce evidence when an assessor or acquiring bank asks for it.

For teams evaluating why these frameworks matter more broadly, this short explanation of the importance of security compliance standards is useful because it connects formal controls to practical business outcomes.

Strong PCI hosting gives you a platform for compliance. It does not replace the management system that keeps that platform compliant.

The Shared Responsibility Matrix You Cannot Ignore

The fog usually shows up in contracts and onboarding calls. The provider says the environment is secure. The merchant assumes that means the payment workflow is covered end to end. Then nobody writes down who owns patching inside the application, who reviews remote access, who signs off on script changes, or who keeps evidence for audits.

That's a governance failure, not a firewall failure.

73% of SMBs can't locate explicit PCI DSS responsibility clauses in their hosting contracts, and 60% of hosting providers lack current Attestation of Compliance documentation, according to VikingCloud's analysis of TPSP and merchant responsibility under PCI DSS. That should change how you evaluate every provider conversation.

PCI DSS Shared Responsibility Matrix Merchant vs. ARPHost

| PCI DSS Requirement Area | Merchant Responsibility | ARPHost Responsibility (Unmanaged) | ARPHost Responsibility (Fully Managed) |

|---|---|---|---|

| Network architecture scope | Define which systems are in PCI scope and which apps handle cardholder data | Provide infrastructure capable of segmentation and secure deployment | Assist with infrastructure design and operational alignment for scoped environments |

| Firewall rule intent | Approve business-justified flows for payment apps and admin access | Maintain provider-side network availability and base connectivity | Implement and maintain agreed firewall policy on managed systems |

| Operating system patching | Patch self-managed servers and any application stack the merchant controls | Deliver the server or VM platform | Handle managed OS patching and routine maintenance where included |

| Application patching | Update ecommerce platform, plugins, payment modules, custom code, and third-party integrations | Not responsible for merchant-installed apps | Support patch workflows if the application layer is part of the managed scope |

| Encryption use | Ensure applications use secure payment workflows and proper data handling | Provide infrastructure that supports encrypted services | Help configure managed services to align with secure transport and storage practices |

| User access approvals | Decide who should have access, review role necessity, remove stale accounts | Provide account mechanisms for purchased services | Enforce managed account practices and support access reviews |

| Logging review | Review security-relevant events and escalate anomalies | Provide system access and platform support | Assist with centralized monitoring and operational review on managed systems |

| Vulnerability scanning coordination | Run required scans, remediate findings in merchant-controlled layers, submit evidence when needed | Maintain the host platform | Help remediate findings in managed infrastructure layers |

| Third-party scripts | Inventory and validate scripts on payment pages | No ownership of merchant marketing or analytics scripts | No ownership unless explicitly contracted for application-level management |

| Incident response | Lead business response, customer communications, legal coordination, and merchant-side evidence gathering | Support infrastructure incident handling within provider scope | Coordinate closely on managed systems and provide operational evidence from covered services |

| Physical security | Verify provider controls and documentation | Maintain data center and hardware access controls | Same as unmanaged |

| AOC review and vendor oversight | Obtain and review current provider documentation | Provide available compliance documentation for covered services | Same as unmanaged, with clearer support through managed relationship processes |

Where responsibility actually breaks

A few examples make this more concrete.

If you run WooCommerce, Magento, or a custom checkout app on a VPS, the host can deliver a hardened virtual machine, secure hypervisor isolation, and protected facility access. But if your team leaves an outdated extension in place, PCI exposure remains yours.

If the provider offers MFA for admin access but your team creates broad access groups and never removes former contractors, that's also on you.

If a marketing team adds a script to the payment page without security review, “PCI hosting” won't save the audit finding. The provider didn't approve the change. Your business did.

What a good contract should state

Look for direct language on these points:

- System boundary clarity: Which layers the provider secures, and which layers remain customer-managed.

- Patch ownership: Separate infrastructure patching from application and plugin patching.

- Log and evidence access: How long logs are kept, how you retrieve them, and who reviews them.

- Incident duties: Who notifies whom, within what timeframe, and who supplies supporting artifacts.

- AOC status: Whether the provider has current compliance documentation for the services you're buying.

If a provider can't describe the boundary in writing, the boundary will fail in practice.

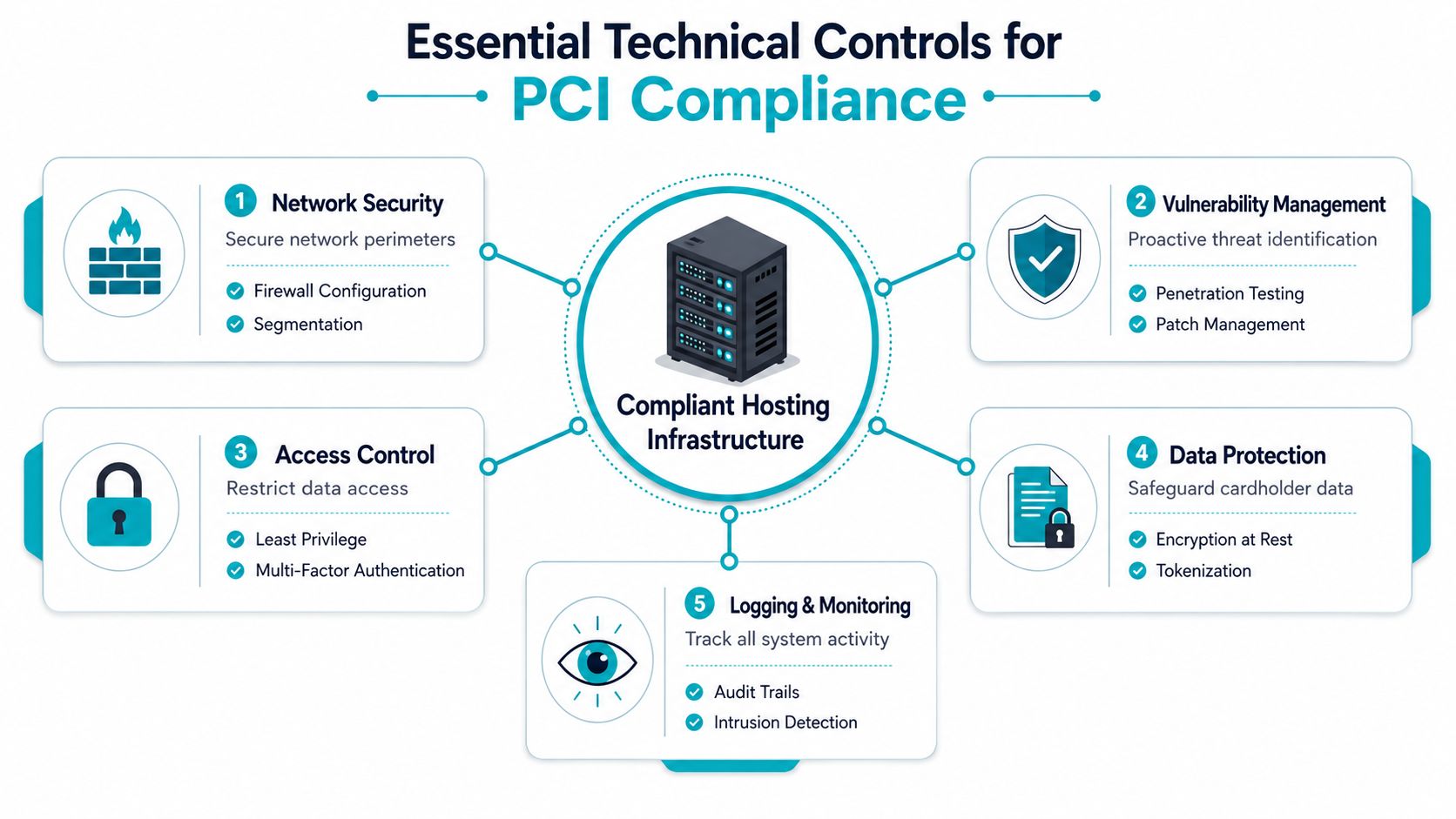

Essential Technical Controls a Compliant Host Provides

A PCI-capable host has to do more than offer a private server and say it's secure. The environment needs controls that support PCI requirements in a way an assessor can recognize and an operations team can maintain.

The first control I check is segmentation. Compliant hosting infrastructure must place the cardholder data environment inside a DMZ, prohibit direct public access from the internet to any CDE component, and enforce default-deny firewall rules that permit only essential connections, as outlined by PXP's explanation of PCI-compliant hosting architecture.

Network separation is the first hard line

Think of the CDE as the vault. Public web traffic shouldn't walk straight into it.

A practical design usually places internet-facing services in a separate zone, then restricts traffic into the payment environment to the exact ports, systems, and workflows required for business operations. Teams that need a plain-language refresher on network segmentation will find that concept easier to evaluate once they map it to payment paths, admin paths, and logging paths.

Useful questions include:

- Can this environment isolate the payment application from the rest of the estate?

- Do firewall rules start from deny-all and then allow only approved flows?

- Can shared tenants be technically separated so one customer can't affect another?

Access, encryption, and visibility

PCI-capable hosting also needs strong access control, secure configurations, vulnerability management, and enough logging to reconstruct events.

A baseline checklist should include:

- Encryption support: Infrastructure and software should support strong encryption for data in transit and at rest, including options such as AES-256 or RSA 2048 as noted in Sprinto's summary of PCI compliant hosting controls.

- Firewall review cadence: Under Requirement 1, organizations must review firewall and router configurations every six months and restrict untrusted traffic to only necessary protocols, according to Onspring's PCI DSS quick guide.

- Logging and monitoring capability: The environment should support centralized collection, alerting, and review, not just raw log files dumped on disk.

- Malware and file integrity controls: Website and server environments benefit from tools that can detect tampering, malicious uploads, and suspicious changes.

For a layered explanation of how infrastructure security should stack from edge to workload, this piece on security in layers is a useful operational reference.

A host that can't explain segmentation, access boundaries, encryption support, and log visibility in technical terms is not ready for PCI conversations.

Choosing Your Hosting Environment for PCI Compliance

Not every hosting type is a sensible home for payment processing. Some environments are fine for brochure websites that redirect users to an external payment processor. Others are suitable for applications that process cardholder data directly. The difference is isolation and control.

Shared hosting, VPS, bare metal, and private cloud

Here's the practical view.

Shared hosting

Shared hosting is usually the weakest fit for in-scope card processing. Even when the provider isolates accounts well, you still have limited control over segmentation, logging depth, custom security tooling, and administrative boundaries.

It can still work for low-risk web presence use cases where the site doesn't process or store cardholder data directly and instead hands payment off to a specialized processor. In that design, the website's job is to stay clean, patched, and separated from the payment workflow.

VPS hosting

A VPS is the entry point for serious control. It gives you OS-level authority, clearer boundaries, and room for hardened configurations.

The trade-off is responsibility. If you choose unmanaged VPS for a payment workload, your team owns far more of the patching, monitoring, and hardening work. That's often acceptable for experienced operations teams. It's risky for understaffed IT groups who already struggle with routine maintenance.

Bare metal

Bare metal is where PCI designs become much easier to reason about. You remove noisy multi-tenant concerns, gain full control over segmentation and monitoring, and can dedicate hardware to the payment environment.

For example, a high-memory system like the AMD EPYC 4584PX with 16 cores, 32 threads, and 192GB DDR5 RAM is well suited to isolated private cloud builds, larger databases, and dense virtualization stacks when a merchant needs strict separation and predictable performance. A compute-dense option like the Dual Intel Xeon E5-2690 V3 with 28 cores and 56 threads is useful for Proxmox clusters or multi-system PCI segmentation on dedicated hardware.

Private cloud

A dedicated private cloud is often the cleanest answer for merchants that need multiple workloads with strong separation. You can isolate web, application, database, jump host, and logging functions while keeping them inside an environment you control operationally.

That's especially attractive when the business needs more than a single PCI server. It allows structured segmentation without mixing the payment estate into general-purpose infrastructure.

Match the payment design to the hosting choice

If you're deciding whether to keep payments off-site or process them within your own application, it helps to first compare SA ecommerce payment options and understand what your gateway model means for system scope.

For organizations that need dedicated infrastructure, migration flexibility, or hybrid deployment options, colocation and hosting environments can support a more controlled PCI design than generic retail hosting.

What works in practice

A good rule set is simple:

- Use shared hosting for marketing sites or simple storefronts that offload payment handling completely.

- Use VPS when you need application control but can still keep the PCI footprint narrow.

- Use bare metal when you want direct hardware isolation and easier audit boundaries.

- Use private cloud when the payment environment spans several systems and needs disciplined segmentation.

The wrong choice isn't always the cheapest one. It's the one your team can't securely operate.

How to Vet and Validate Your Hosting Provider

The right provider should welcome hard questions. If sales gets evasive the moment you ask for documentation, control details, or scope boundaries, move on.

The first two things to validate are identity and evidence. PCI-capable hosting must require MFA for all non-console administrative access into the CDE, and systems must retain audit trail history for at least one year, with at least three months immediately available for analysis and every action linked to a unique user ID, according to Atlantic.Net's overview of PCI compliance requirements.

Questions that expose weak providers

Ask these directly:

Can I review your current AOC for the services I'm buying?

A good answer is specific. It identifies the covered service, the date, and what parts of the stack are in scope.Where is the customer-provider responsibility boundary documented?

You want a written matrix, not verbal reassurance.How is administrative access protected?

Listen for MFA, unique IDs, role separation, and session accountability.What audit logs are retained, for how long, and how do customers access them?

A weak answer says logs exist. A strong answer explains retention, availability, and export or integration options.How do you support segmentation and restricted network flows?

The answer should mention DMZ-style separation, firewall policy control, and isolation options.Who patches what?

This question surfaces hidden assumptions faster than almost any other.

What a strong answer sounds like

A serious provider speaks in layers. They can explain physical controls, virtualization boundaries, access enforcement, log handling, and where the customer must still act. They won't claim your business becomes compliant by default.

They'll also know whether your workload should live on shared hosting, a managed VPS, dedicated hardware, or a private cloud. If they try to force every PCI use case into one generic package, they're optimizing sales simplicity, not your risk profile.

Why ARPHost excels here

A strong benchmark provider offers both unmanaged and managed models, dedicated hardware, virtualized environments, and clear escalation paths. That matters because PCI needs flexibility. Some teams need root control. Others need hands-on operational help.

It also helps when the same provider can support adjacent regulated environments. If you're comparing how a host handles protected workloads more broadly, reviewing its approach to HIPAA-compliant hosting can tell you a lot about documentation discipline, access control maturity, and managed service depth.

Ask every provider one uncomfortable question: “Show me the document that proves this claim.” The good ones won't flinch.

Your Path to Sustained Compliance with ARPHost

PCI DSS compliant hosting is a foundation, not a finish line. The durable approach is to pair the right environment with clear ownership, documented procedures, controlled change, and regular validation. That's how teams stay out of the shared-responsibility fog.

If you process payments directly, choose infrastructure that gives you isolation and operational clarity. If you have a small internal team, don't pretend unmanaged infrastructure is cheaper if it leaves patching, logging review, and incident coordination unfinished. If your payment stack spans several systems, design for segmentation from the start instead of trying to bolt it on later.

ARPHost is well positioned for that kind of work because the platform options align to real PCI use cases. Their VPS hosting supports teams that need control. Their bare metal inventory fits isolated payment workloads and private cloud builds. Their dedicated Proxmox private clouds make sense when you need segmented systems on dedicated hardware. Their fully managed IT services help close the gap between secure infrastructure and secure operations.

For many merchants, that combination is what finally makes PCI manageable. Not automatic. Manageable.

If you need an infrastructure partner that can support secure payment environments without hand-waving the shared-responsibility details, ARPHost, LLC is a strong place to start. Explore VPS hosting for controlled application deployments, review bare metal servers for isolated CDE designs, compare Proxmox private clouds for segmented multi-system architectures, or request fully managed IT services if your team needs help with patching, monitoring, and day-to-day security operations.